Benefiting from a more diverse value proposition in global bond markets

While inflation risks and fiscal worries keep yields in the US higher, CHF bond investors are once again facing the challenge of low or even negative yields. Investors can benefit from a more diverse value proposition in global bond markets. Nonetheless, robust and proactive risk management in terms of duration, credit and currency exposure will be essential to protect and grow client wealth.

| Dario Messi, CFA Head of Fixed Income Research, Bank Julius Baer & Co. Ltd. |

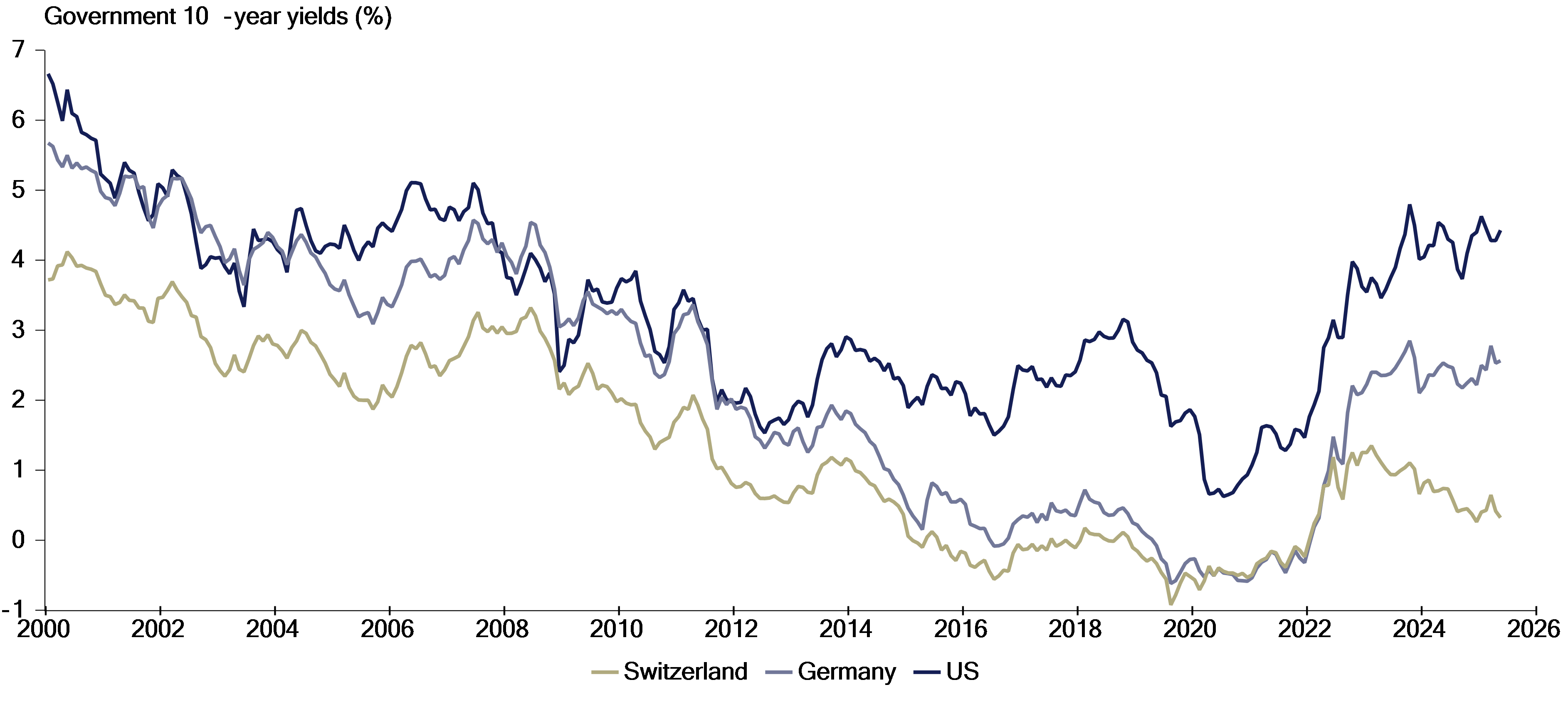

Where we stand: a tale of two (or multiple) speeds

The memory of 2022's brutal repricing in bond markets still lingers among investors, who recall how central banks worldwide combated the inflation surge by hiking policy rates into restrictive territory, causing rates and yields to spike globally. However, this significant shift also produced a silver lining: the concept of yields serves as a good starting point for modeling forward-looking return potential in bond markets. In essence, the price reset ultimately created an opportunity for investors to reinvest at nominally better levels, including more cushioning. Since then, the global bond market has become increasingly complex, exhibiting diverging dynamics that make navigation particularly challenging for CHF-based investors. In the US, for instance, the Federal Reserve has adopted a cautious stance following the initial rate cuts in late 2024. Moreover, longer-dated bond yields remain elevated due to concerns over erratic policy out of Washington, ongoing inflation risks, consistently high fiscal deficits, and more structurally, a desire to diversify away from USD assets. In contrast, Switzerland's sub-target inflation and strong currency have pressured the Swiss National Bank (SNB) to opt quickly for relatively low policy rates again. Indeed, at the time of writing [End June 2025], the SNB just lowered its policy rate to 0%, and further decreases into negative territory are well possible, already reflected in the Swiss government curve, where short to medium-term yields have dipped below 0%. Naturally, investors are now left wondering how to effectively navigate this environment.

Chart 1: diverging patterns in government yields

Source: Macrobond, Julius Baer

Challenges arise when we hit the lower bound

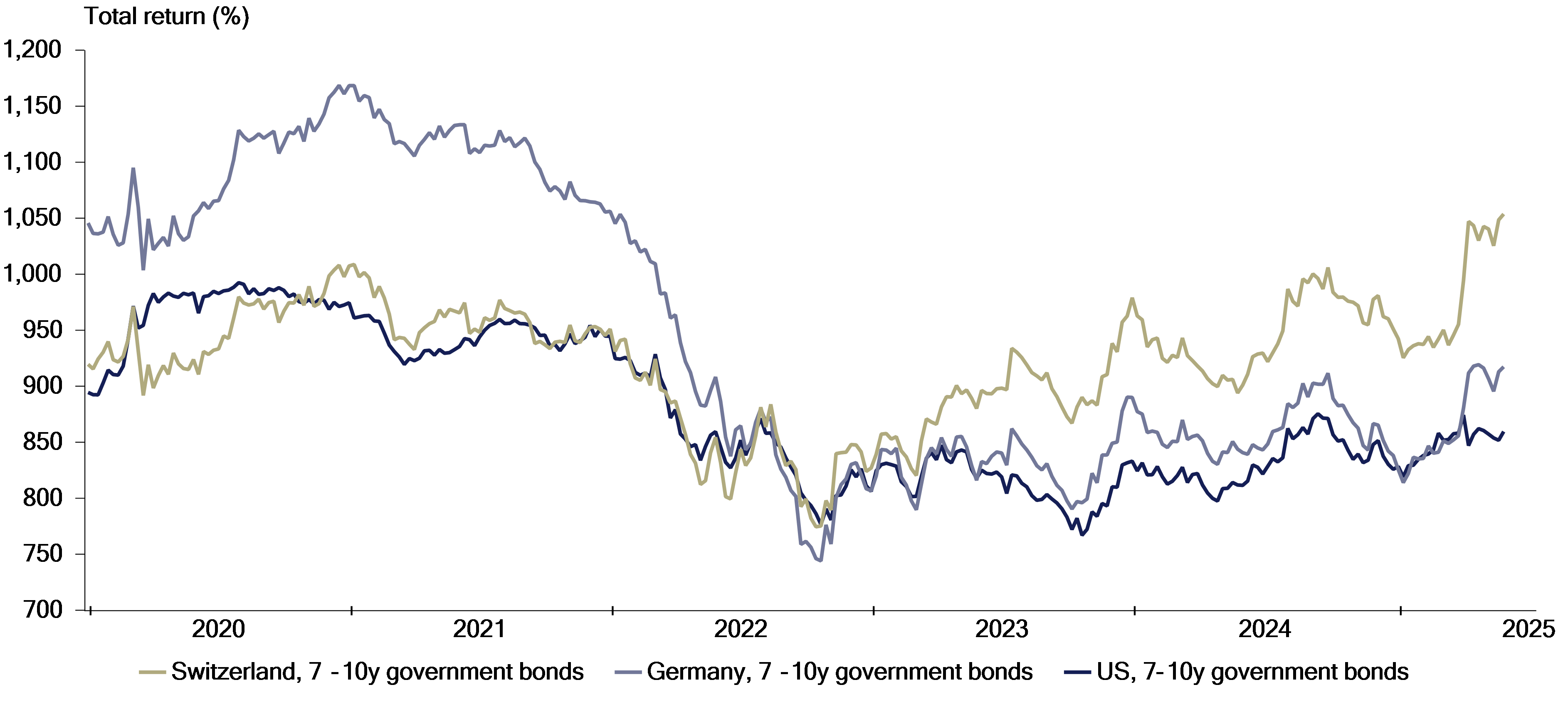

From a CHF-based portfolio perspective, the fixed income allocation has once again become a complex issue. The decline in yields is always a boon for bond investors, delivering capital gains in addition to regular coupon income, with CHF bonds having generated attractive returns since 2023. But the arrival at 0% or even negative yields once again presents a significant challenge. At these levels, new investments offer minimal carry income. Achieving similar positive returns as in the past requires speculating on further yield declines, deep into negative territory, which limits forward-looking return potential and creates asymmetric risks. CHF-based investors currently find themselves in this predicament. To navigate this environment, portfolio managers, especially those overseeing private wealth, can take several steps.

First, investing in negatively yielding bonds should be avoided whenever possible. Of course, this is easier said than done, as it typically involves increasing either duration or credit risks, making proactive risk management essential. Exploring alternative segments can certainly be very beneficial in such circumstances. In particular, domestic Swiss real estate can help mitigate the adverse effects of negative real yields and provide better return potential, while being better equipped to hedge against the erosion of purchasing power. Another option is to explore cross-border opportunities, which significantly expand the investment universe and therefore the opportunities to enhance the starting yield. The access to segments with higher credit spreads, such as USD and EUR-denominated corporate credit markets or emerging market debt further enhance the potential for carry income. Nonetheless, it is crucial to acknowledge that the risk profile of such investments alters. More importantly, when venturing into cross-border investments, the question of currency hedging inevitably arises, adding another layer of complexity to the decision-making process.

Chart 2: CHF bonds performed better as capital gains returned quickly

Source: ICE indices, Macrobond, Julius Baer

Ultimately, it’s about knowing the asset’s role in portfolios

In general, fixed income investments are best conducted on a currency-hedged basis, as exchange rate fluctuations can overshadow coupon income and undermine the fundamental characteristics of bonds. These are providing a stable income stream and, in the case of safer bonds, offering hedging properties during times of market stress. There are exceptions, however, for example when non-CHF based investors deliberately hold CHF bonds without currency hedging, leveraging the strong Swiss currency to add stability and hedging benefits to their portfolios. After all, the combination of low yields and a strong currency in Switzerland is no coincidence, but rather a reflection of the country's robust governance and political stability. This has created an ideal environment for storing value and wealth, particularly in today's climate. Conversely, CHF investors may be willing to assume moderate currency risks when investing in higher-yielding segments like emerging market debt or USD and EUR corporate debt, as the increased yield provides a buffer for any potential adverse currency impact. Ultimately, it is crucial to consider each portfolio component in context and understand its intended role, with currency hedging decisions being paramount, especially for bond allocations.

In conclusion, investors can capitalize on the diverse value propositions presented by different bond markets and currencies, but apart from careful consideration and strategic decision-making, this requires a clear understanding of each asset’s role in the portfolio context.

Biography

As head of the Julius Baer Fixed Income Research team, Dario Messi is responsible for the global fixed income strategy recommendations, using a top down perspective. He contributes to Julius Baer’s Investment Committee and the Bank’s Asset and Liability Management Committee. Dario joined Julius Baer as a fixed income strategist in 2016. His areas of expertise include the interaction between the financial market and the real economy, with a focus on monetary policy and credit segments. Dario Messi holds a Master’s degree in Economics from the University of Zurich and is a CFA charterholder.