AI and demographics: the economic tug of war

The US Federal Reserve Board released its longer-run economic projections[1] in March 2024, offering insights into the future of the US economy. However, the consensus view that the future of the world’s largest economy will resemble its recent past may be misguided.

| Jonathan Decurtins, Senior Sales Executive, Vanguard Investments Switzerland GmbH |

The Federal Reserve Board’s projections, which were supported by similar insights released by the US Congressional Budget Office (CBO), include:

- Real economic growth between 1.6% and 2.5% per year—a percentage point less than the growth rate since World War II.

- Annual inflation of 2%.

- Short-term interest rates between 2.4% and 3.6%, well below their current level.

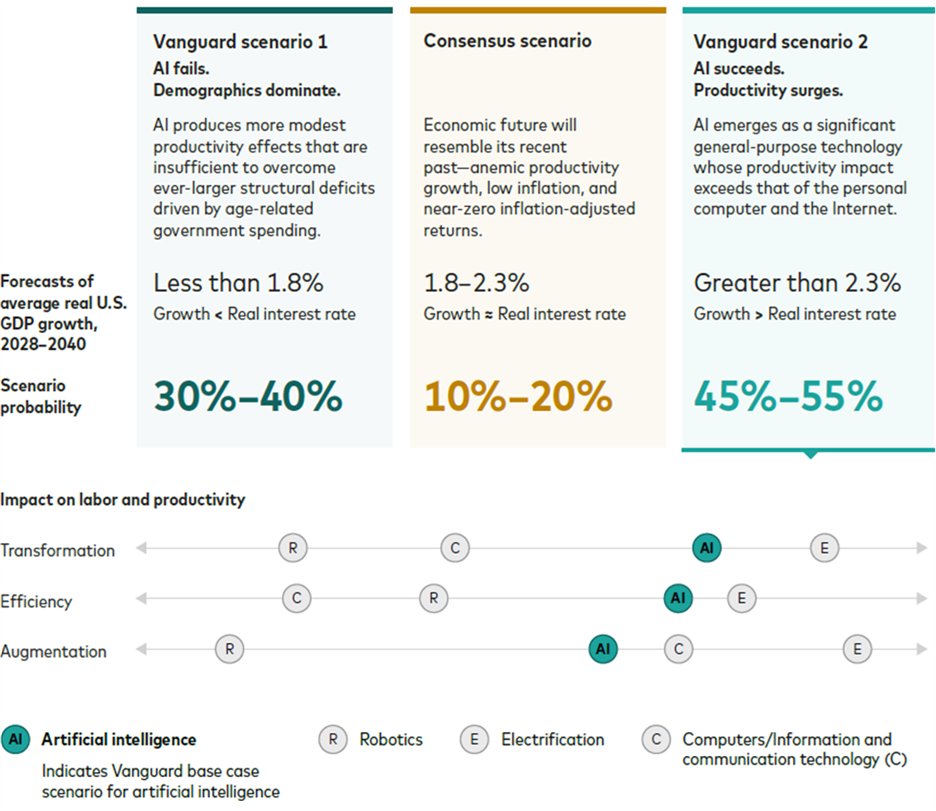

The broad economic consensus is that our economic future will resemble the recent past—anaemic productivity growth, low inflation and near-zero inflation-adjusted returns on government debt.

Our analysis suggests otherwise: we give this scenario a 10%–20% likelihood. The most likely outcome in our view, with a probability of 45%–55%, is that artificial intelligence (AI) catalyses a surge in economic growth.

The next most likely outcome, at 30%–40%, is that AI fails to meet our expectations. In this scenario, a slow-growing, ageing population fuels government deficits and debt that limit growth and improvement in living standards.

A new megatrends forecasting framework

These projections are the output of Vanguard’s novel economic forecasting framework. The model integrates the short-term business-cycle variables that drive most economic forecasts with the slower-moving supply-side forces that determine an economy’s productive capacity over decades. These megatrend forces include demographics, technological change, deficits and globalisation.

Our analysis indicates that the future of the global economy depends on a tug of war between AI and demographics-driven deficits. The stronger of these two forces will determine the economic and financial outcomes that matter to workers, investors and policymakers.

Age-related spending and structural deficits

The US government ran a primary surplus in 141 of the 208 years between 1792 and 1999, almost 70% of the time. (A primary surplus means that tax revenues exceed government spending, excluding interest payments on the debt.) More recently, this pattern has flipped. The US recorded primary deficits in 20 of the 24 years between 2000 and 2023 (83%).[2]

The US government's shift from surpluses to deficits can be attributed to an ageing population, which has led to increased spending on healthcare and social security. These structural deficits, coupled with rising interest rates following Covid-19, pose a threat to economic growth and raise concerns about inflation and borrowing costs. According to CBO estimates, by 2054 the ratio of US debt to GDP will exceed 170%, up from about 100% today.

However, emerging technologies, particularly AI, hold the potential to boost economic growth and mitigate the impact of age-related spending.

The AI productivity opportunity

Technological innovation has historically been the primary driver of productivity growth and improvements in living standards. Vanguard's research highlights three key aspects of technological innovation:

- General-purpose technologies (GPTs) such as electricity and the computer.

- Automation of routine tasks that free workers to focus on more valuable work.

- Labour-augmenting innovations such as power tools.

The conditions for the emergence of GPTs are present today, with increased capital investment in new technologies and sluggish productivity growth. If AI's impact matches that of electricity, it could offset demographic pressures and exceed consensus expectations for economic and financial outcomes.

But if productivity gains mirror those delivered by robotics, computers and the internet, demographics will dominate. Economic and financial outcomes will fall short of consensus estimates.

Sizing the odds: demographics vs. AI

Vanguard's research presents two scenarios for the future. In the first, most likely scenario, AI emerges as a significant general-purpose technology, surpassing the productivity impact of the personal computer and the internet. In the other scenario, AI fails to meet expectations, leading to modest productivity effects that are insufficient to overcome structural deficits driven by age-related government spending.

Source: Vanguard.

Notes: We define transformation as a shock to the diffusion of general-purpose technology, efficiency as a shock associated with automation, and augmentation as a labour-augmenting shock where both output and employment rise simultaneously.

The eternal tug of war

Technology and demographics have always competed, as Thomas Malthus articulated in An Essay on the Principle of Population (1798). He argued that population growth would lead to war, famine and disease. In 1798, the earth’s population totalled 800 million. But in 2022, 8 billion people inhabited a richer, healthier planet. Technological progress neutralised the Malthusian warning: “The power of population is indefinitely greater than the power in the earth to produce subsistence for man.”

Yet the tug of war continues. Today, the struggle is between a slower-growing, ageing population and our capacity to improve, or even maintain, living standards. As economist Ester Boserup observed, however, “necessity is the mother of invention.” We expect technology to prevail—we’ll innovate faster than we age.

Read the full report, Megatrends and U.S. Economy, 1890–2040, here.

[1] The Fed doesn’t specify a time frame for “longer-run projections,” noting only that it represents the Federal Open Market Committee members’ “assessment of the value to which each variable would be expected to converge, over time, under appropriate monetary policy and in the absence of further shocks to the economy.”

[2] Sources: Vanguard calculations, based on government spending and outlay data from the Global Financial Database (for 1792–1961) and the Congressional Budget Office (1962–2023).

Biography

Jonathan Decurtins is a Senior Sales Executive with responsibility in wholesale distribution and independent wealth managers in the German- and Italian-speaking regions of Switzerland as well as Liechtenstein. He joined Vanguard in 2022 from Zürcher Kantonalbank, where he was a relationship manager responsible for serving clients domiciled in the United Kingdom. Prior to that, he spent three years at Invesco as ETF Sales Manager for Switzerland and Liechtenstein. Before moving to Invesco, Jonathan worked as a relationship manager for index solutions at RobecoSAM and as an investment consultant for index funds in asset management at Zürcher Kantonalbank. Jonathan holds a Master of Advanced Studies in Applied History from University of Zurich as well a Professional Bachelor degree in Banking and Finance from Höhere Fachschule Banking & Finance in Zurich.

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Important information

For professional investors only (as defined under the MiFID II Directive) investing for their own account (including management companies (fund of funds) and professional clients investing on behalf of their discretionary clients). In Switzerland for professional investors only. Not to be distributed to the public.

The information contained herein is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information does not constitute legal, tax, or investment advice. You must not, therefore, rely on it when making any investment decisions.

The information contained herein is for educational purposes only and is not a recommendation or solicitation to buy or sell investments.

Issued in Switzerland by Vanguard Investments Switzerland GmbH.

© 2024 Vanguard Investments Switzerland GmbH. All rights reserved.